The problem you will find when searching for insurance online is that most quote journeys and policies are standard home insurance.

The default for these providers is that ownership options are a person or a business:

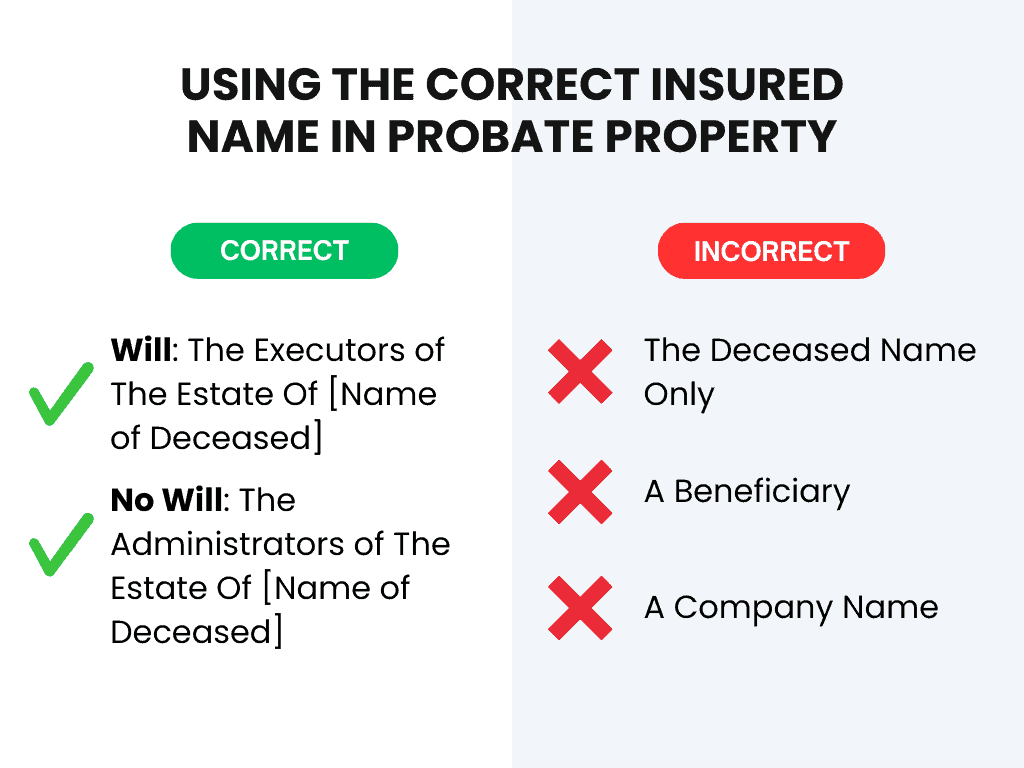

The Name of the Insured for Probate should be either:

If the property is owned as tenants in common, you can add to the end of this “and [name of the other owner]. This can arise when the surviving spouse is in care.

What the Insured's name shouldn’t be:

Using “Executors or Administrators of” means anyone in that role, as listed in the Will or the Letters of Administration, can be involved in the administration of the insurance policy, handling any claims, and receiving claim settlements on behalf of the estate.

In about 30% of cases, properties are owned as Tenants in Common rather than Joint Tenants. This is common in second marriages or where families are protecting assets from care home fees.

In this scenario, the deceased’s share doesn't automatically pass to the survivor; it stays with their estate. Therefore, the insurance must reflect both legal owners.

So in this scenario, here is the correct Insured Name:

Using this format ensures:

The Survivor is protected for their share of the property.

The Estate (and its beneficiaries) is protected for the deceased’s share.

Insurable Interest is correctly described, ensuring there are no disputes during a claim, which is the last thing a family needs when one partner is already dealing with probate or moving into care.

Under the Administration of Estates Act 1925, the estate is a separate legal entity.

By insuring as "Executors or Administrators of," you correctly identify the group with the legal right and duty to protect the property.

If a policy remains in the name of a deceased person, it is technically a contract with someone who no longer exists, which can cause problems when it comes to a claim.

If the policy is in the name of a beneficiary who has yet to become the legal owner, they effectively have no insurable interest in the property, which could void the policy.

To make this easy for you, we remind you of the correct naming convention when you are requesting a quote. Just follow the instructions on the screen to ensure it is done correctly.

Whether you insure with Insuristic or not, this should help you with whichever provider you choose.

To find out more about our cover or get a quote, visit our Probate House Insurance page. If you have further questions, visit our Probate Insurance FAQs page.

Rob Faulkner is a leading expert in Probate Insurance, Probate Risk Management, Property Insurance (especially Unoccupied Home Insurance), with nearly 30 years’ experience in the UK insurance market. He is the founder of Insuristic, a specialist provider of probate-related insurance solutions and educational content for executors.

Rob is an ACII Chartered Insurance Broker, a Chartered Manager, and a Member of the Chartered Institute of Marketing. His background spans insurers, brokers, and Insurtechs, always focused on innovation, transparency, simplicity, and fair value.

Rob is passionate about product development and improving insurance education through marketing, helping people understand what they are buying. These values sit at the heart of everything we do at Insuristic.

His mission is to make Insurance smarter, easier to understand, and faster to buy. Particularly for the Probate market, where Rob has identified friction points and solved them for lay clients and solicitors alike.

Want to learn more? Visit my author page or follow me on LinkedIn.

Insuristic Limited is an Appointed Representative of SJL (Worcester) Ltd, who are authorised and regulated by the Financial Conduct Authority with the reference number 991835. This can be checked by visiting https://register.fca.org.uk/s/.

Registered Office: Unit 2, 262 Walsall Road, Cannock, England, WS11 0JL. Registered in England and Wales No: 13926650.

Insuristic is a registered trademark. ©Copyright 2023 Insuristic Limited. All Rights Reserved.