This policy was designed by our founder, Rob Faulkner, an ACII Chartered Insurance Broker with 30 years' experience in the UK insurance market.

After going through probate himself, he saw how many policies leave personal representatives exposed, including limited cover, weekly inspections, policy adjustment and cancellation fees, and pro-rata refunds rarely offered.

He built this insurance policy to fix that: broad cover options, underwritten at Lloyd's, exclusive to Insuristic, with no fees for changes or cancellation, and a pro-rata refund if the property sells sooner than planned, provided no claims have been made.

Our policy is exclusively available from Insuristic. It has been designed specifically for empty property in probate and is suitable for any stage of the probate process.

If you need help, start an online chat or contact us. Please note that during busy periods or outside of office hours, we will reply to your questions via email as soon as possible.

Why not also see what our customers think of us on our Trustpilot page?

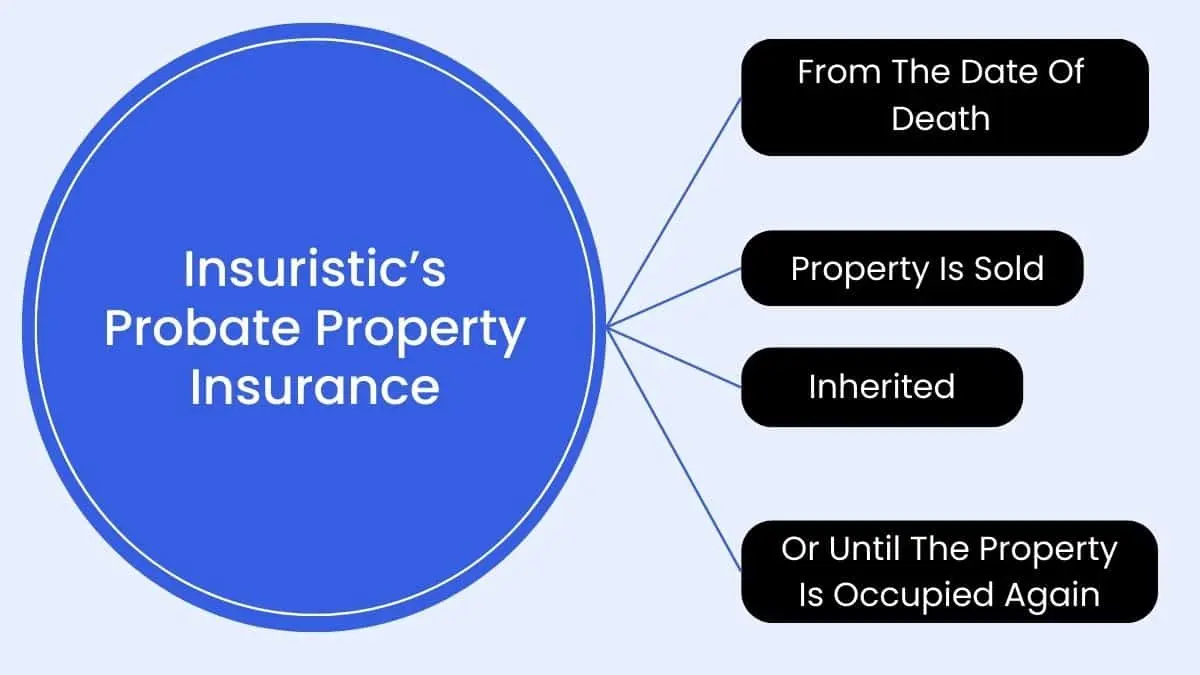

Probate House Insurance is specialist cover for an empty property going through probate. It protects executors and administrators from personal liability for the property while the estate is being settled — from the moment it becomes empty until it's sold, transferred to a beneficiary, or occupied again.

Many insurance providers offer general unoccupied home insurance policies (as do we for properties not in probate), but these policies may not adequately address the unique challenges of insuring an empty property during probate.

Insuristic understands the complexities of this situation. Our founder, Rob Faulkner, an ACII Chartered Insurance Practitioner, personally experienced the frustrations of navigating probate and developed our specialised Probate House Insurance policy to help others in similar situations.

Our cover can start as soon as the property becomes vacant, as this marks the start of the probate process, even if you have not yet started the application. The cover ends when the property is sold, inherited or occupied again.

Our approach eliminates the risk of cover ending suddenly once you receive confirmation of Probate (which is a risk with some insurance providers).

As an executor, administrator, or personal representative, you have a legal responsibility to protect the deceased’s property until it is passed to the beneficiaries.

This is an emotional time, and the last thing you need is added financial stress. However, if you fail to insure the property correctly, you may be held personally liable for any uninsured or underinsured losses.

Your Liability Risk

If a loss occurs and the insurance is inadequate, the financial shortfall often falls on the executor’s or administrator's shoulders. For example:

Choosing the right house insurance for probate is one of the most important decisions a personal representative makes.

Insuristic makes it quick and easy to arrange Probate Home Insurance online.

As a UK-based specialist insurance broker, we offer probate home insurance across England, Scotland and Wales.

Many providers offer generic unoccupied policies designed for short-term gaps between tenants. These are built to protect the insurer, not the executor.

Standard policies often include cover restrictions that increase your risk:

This is why home insurance for probate property needs to be evaluated carefully — the unique risks executors face require a more specialist policy than a standard unoccupied product.

Most of our customers are worried about their personal liability when insuring a probate property. This page covers the key things you need to know about the cover, conditions, and pricing, but this section explains what it's like to insure with us. We cover the process of getting a quote, comparing cover, renewing, spreading the cost and claiming.

You can usually arrange probate property insurance online in a few minutes. Your quotes and policy documents will be emailed to you immediately.

If you aren’t ready to buy, you can log in to our secure portal to review your quotation history, buy a policy and retrieve your policy documents.

If your quotation refers to the underwriter, don't worry. Our underwriters will contact you to provide advice and options from multiple insurers, ensuring the policy is correctly insured in the name of the estate and provides cover to meet your needs.

We know you have a lot to consider, particularly when it comes to protecting your personal liability as a personal representative. Insuristic’s policy has been designed specifically for this.

This page explains the cover in detail, and you will also receive a reminder of each cover level and its 30-day inspection frequency (which is generally broader than the market provides) throughout the quote journey.

Whilst the estate pays for the insurance, many people in your situation want to compare pricing across cover levels. This is easy to do with Insuristic.

Enter your details once, then click edit your quote on the quote summary page to check pricing for different cover levels. Each quote will be emailed to you to review.

If you need help at any point, start an online chat or visit our customer support page.

We know probate timelines and property sales can be unpredictable. If you are considering a 12-month policy, a shorter term might be the better option, particularly if you want to spread the cost.

You can buy a 3 or 6-month policy and keep extending it for as long as the property remains your responsibility.

We don't charge more for short-term cover. Whichever policy duration you choose, the underlying pricing is the same, just on a pro-rata basis, so you only pay for the cover you need.

If the property sells or the estate settles sooner than expected, just reply to your policy email with the date and reason for cancellation. Provided you haven't claimed, you'll receive a pro-rata refund of the unused premium, with no cancellation fee.

Pro-rata refunds with no cancellation fee are rare in the market; many providers charge a £30-£60 fee and may retain the unused premium.

You will receive a renewal invitation 20 to 30 days before your renewal date. We don't automatically renew your policy, so if nothing has changed and you want to continue cover, log in to our secure portal to pay.

If you no longer need cover, your policy will end on the expiry date, and you'll receive a lapse confirmation by email.

If you need to change the cover level or policy duration, or have questions, reply to your renewal email and we'll send a revised renewal quote you can buy when ready.

As mentioned above, if you need to end cover earlier than planned and haven't claimed, you'll receive a refund of unused premium with no cancellation fee.

If you need to claim, you'll speak directly to our underwriter’s in-house UK claims team, who are available 24 hours a day, 365 days a year. It is not a call centre - you will speak to claims experts.

You will be assigned a dedicated claims manager, so you'll be dealing with the same people from the first call to settlement.

Full claims contact details and a guide to the claims process are below. The claims number will also be on your policy schedule.

When you get a quote from Insuristic, you can:

Don't worry - our online quote system explains this at the time you need to provide the insured name.

We cover this in more detail in our article Whose name should house insurance be in during probate?

Getting a quote from Insuristic is a straightforward process.

However, if you ever need assistance, our dedicated team can be contacted via our online chat.

If, for some reason, your property doesn’t fit our online requirements, such as it has a high value, is in poor condition, is in a flood area or has had recent claims, we can find a solution for you offline once you have completed our online quote form. The same applies if you require advice.

The cost will vary depending on providers, the level of cover you buy, and how long you need to insure the property.

Currently, the average Insuristic customer spends the following, with at least our Silver level of cover (pricing correct between April 2025-26):

| Cover Duration | Probate Property |

|---|---|

| 3 Months | £95 |

| 6 Months | £189 |

| 9 Months | £337 |

| 12 Months | £431 |

We know that probate timelines are unpredictable. You might need cover for a year, or the property might sell much sooner than expected.

Unlike most insurers who charge cancellation fees and limited refunds, we take a much fairer approach:

Unlike many competitors, Insuristic Probate Property Insurance policyholders are not required to create a written inspection report, and our inspection frequency is typically more flexible.

With our policy, properties only need to be inspected once every 30 days. The inspection can be carried out by anyone with access to the property and a mobile phone; it doesn’t have to be the executor.

During each visit, the property must be inspected both internally and externally. To document the inspection, the person conducting it should take one photo of the front of the property and one inside to confirm entry.

In the event of a claim, the underwriter's claims team will require these photos as evidence.

To reduce the risk of fire or explosion, most insurers require utilities (gas and electricity) to be switched off at the mains while the property is unoccupied (you can switch them on during your visits - just ensure you switch them off again when you leave).

However, there are two important exceptions to this rule:

Failure to switch off unused utilities as required by your policy may result in a claim being declined if an avoidable incident occurs.

Burst pipes are the most common cause of significant damage in probate property. To maintain your cover for Escape of Water (available on our Silver and Gold cover), you must choose one of the following two options:

Option A: Drain the System. This is the safest way to eliminate risk. You must turn off the water at the mains (stopcock) and professionally drain the entire water and heating system. If the system is fully drained, full cover for Escape of Water is typically maintained.

Option B: Keep the Heating On (Winter Condition). If you prefer not to drain the system, you must ensure the property is heated to a constant temperature (usually 15°C) at all times between October 1st and March 31st. Additionally, you should leave the loft hatch open to allow warm air to circulate into the roof space, where pipes are most vulnerable to freezing.

See the cover levels below for details on the amount of cover we provide.

Our insurance policy offers three levels of cover, Bronze, Silver or Gold.

Executors should consider the level of risk they are prepared to take and choose the most suitable insurance policy.

Most executors choose to buy at least our Silver cover.

Here is an overview of each cover level:

Bronze is our basic level of cover. It only covers loss or damage to the buildings (or contents if you have chosen to insure that) caused by:

Fire

Lightning

Explosion

Earthquake; or

Aircraft

This cover is often referred to as FLEEA Insurance cover.

In addition, level 1 also includes:

Architects & Surveyor's fees and debris removal

Property owners liability insurance, covering your legal liabilities up to £2,000,000 should a member of the public be injured or have their property damaged at your premises.

Exclusions will be found in your Insurance Product Information Document (IPID) or policy wording.

Extends the cover provided by Bronze to also include:

Subsidence, flood, vandalism, escape of water and theft

£3,500 cover for claims caused by malicious damage, escape of water or theft.

Full escape of water cover if the system is drained down.

Please note:

The maximum amount payable for claims is the sums insured listed on your policy schedule.

If water systems cannot be drained, the maximum amount payable for an escape of water claim is £3,500 and this is providing that you keep the heating to a minimum temperature of 15° Celsius between 1st of October and 31st March and, where fitted, must keep the loft hatch open.

Gold is our highest level of cover.

It extends the cover included in Silver, removing the £3,500 claims cap on malicious damage, escape of water or theft claims.

Please note:

The maximum amount payable for claims is the sums insured listed on your policy schedule.

If water systems cannot be drained, the maximum amount payable for an escape of water claim is £5,000 and this is providing that you keep the heating to a minimum temperature of 15° Celsius between 1st of October and 31st March and, where fitted, must keep the loft hatch open.

Executors should take care when comparing probate and unoccupied home insurance policies, as cover levels and conditions vary widely. This guide explains why it's difficult to compare policies and what to watch out for.

If you want to see at a glance what is or isn't covered, please view the IPID (Insurance Product Information Document) for your preferred cover level.

Insuristic is the broker. We handle any administration queries such as requests to cancel, change your policy, renewals etc.

Our Probate Property Insurance scheme is underwritten by SJL (Worcester) Ltd, trading as SJL Insurance Services, on behalf of Lloyd's Syndicate 4444, which is managed by Canopius Managing Agents Limited.

Canopius Managing Agents Limited is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority (Financial Services Register number 204847).

Both Lloyd's of London and Canopius have a longstanding reputation for financial stability and claims excellence. This means that, in the rare event of a claim, you can trust that our underwriting partners will ensure a fair, efficient, and seamless claims process.

SJL Insurance has extensive experience in underwriting property insurance on behalf of these insurers. You will also benefit from their in-house claims expertise, which includes providing advice, arranging loss adjuster surveys, and supporting you through the process to ensure a fair settlement.

We understand that making a claim can be stressful. Our team at SJL Insurance Services is here to support you every step of the way:

Check out our short guide on what is involved in making a claim.

If you are acting as an executor (if there is a Will) or administrator (if there is no Will), you are likely to have many questions. Especially as you may not have insured empty property before.

Arranging insurance during probate is not the same process as arranging standard home insurance, and the cover can differ significantly between insurance providers.

Below are some common FAQs. If we have missed anything you need the answer to, please start an online chat or reply to your quote email with your questions.

If you're unsure whether you need contents cover, consider:

We commonly see contents like old furniture left in the property to make it look lived-in, with little insurable value, so it is perfectly fine not to insure it. It makes the property look lived in, too, which can help reduce the risk of theft and vandalism.

Yes. Our Probate House Insurance gives you the option to insure buildings only, as contents cover is optional, not mandatory.

This makes the policy suitable as probate building insurance when the property is empty of belongings, when valuable contents have been removed to safe storage, or when the executors prefer to manage the contents risk separately.

Yes, you can buy our Probate Property Insurance before probate is formally applied for. In fact, it's recommended as the personal representatives are personally liable for the property from the moment of death, even before the Grant of Probate is received.

Yes, provided the property is still the responsibility of the personal representatives to insure it. It is common for probate to be received and then the property put up for sale, with the proceeds forming part of the estate's distribution, and therefore, the personal representatives are still legally liable for insuring it until this point. If the property is transferred to a beneficiary, the cover will end, and they need to insure it as the new owners.

Yes. Even before Letters of Administration are formally granted, the people applying for them have a responsibility to protect the property. You can buy our policy from the moment the owner has passed away — the cover doesn't depend on the Grant being received.

During probate, the property is your responsibility as a personal representative, and that includes arranging suitable insurance.

Many executors assume the deceased's existing home insurance continues to provide full cover throughout the waiting period, but most insurers either reduce it to basic cover or void the policy entirely once they're notified of the death.

The waiting period for probate applications can take six months or longer, and during that time, any uninsured loss falls personally to the personal representatives.

Specialist house insurance during probate, like our Probate House Insurance, is designed for exactly this situation. Our cover starts from the moment the property becomes empty. It doesn't end automatically when the Grant of Probate is received and runs for as long as the property is in the care of the personal representatives.

Not usually, it is the personal representative's responsibility (the executors if there is a Will and the Administrators if there isn’t a Will). We have seen rare occasions where an executor has lost capacity, and the person with a Power of Attorney or acting as a Deputy, appointed by the Court of Protection insured the property as they were responsible for the affairs of the Executor.

The Insured name in this scenario would still be as we advise on this page, see Whose name should Probate House Insurance be in above.

Yes, provided one of the executors (or administrators) has a UK passport and a UK bank account. If no one has this, then you should consider appointing a UK Solicitor to administer the estate and insure the property on your behalf.

There is no legal requirement to insure a probate property, but the personal representatives are personally liable for any uninsured losses that occur during the administration of the estate. In practice, leaving the property uninsured is a significant personal financial risk.

Read our full guide: Is probate house insurance compulsory?

When someone dies, ownership of their property passes immediately to their estate, and the personal representatives (executors if there is a Will, administrators if there isn't) become legally responsible for it. That responsibility includes insurance.

For a full explanation, read Who owns and insures a house during probate?

Not necessarily. The existing policy may continue for a short period, but the insurer must be notified quickly of the change of risk, and cover is often reduced to a basic level that leaves significant gaps.

Read our full guide: Is a property still insured if the owner dies?

If the probate property is not correctly insured, any uninsured losses, such as gaps in cover or shortfall following underinsurance, pass to the personal representatives to fund, which means the liability for anyone in that role is significant.

If you are concerned about this, you should read the following article, which explains underinsurance in detail: What Is The Risk Of Building Underinsurance In Probate?

There isn’t a specific policy called Executor Insurance, it is a marketing term used to pull together the various insurance policies that the personal representatives should consider. If you mean insuring on a specialist Probate Property Insurance policy, then yes, these policies can help protect the significant liabilities you have in this regard. There are other insurance policies that you should consider when you have probate, such as Early Distribution Insurance, Section 27 Insurance, Missing Will Insurance and Missing Beneficiary Insurance.

Recommended Reading:

When the owner sadly passed away, their existing insurance may suddenly become less effective at protecting your liability, so it needs to be reviewed urgently. All insurance policies have a 7-day change-of-risk notification condition; failure to notify them could invalidate the policy. If they do continue to offer cover, it is often on a basic FLEEA basis (Fire, Lightning, Explosion, Earthquake and Aircraft damage), which leaves big gaps in cover for common claims like burst pipes, theft and malicious damage, plus major claims like flood – the costs of which would pass to the personal representatives to fund if not insured.

Read our articles to learn more:

When the owner has sadly passed away, they cease to be a legal entity and ownership passes to their estate. The personal representatives are immediately responsible for the protection of the property and its insurance, which is why the insured name needs to be the Executors of, or the Administrators of, the estate of [name of the deceased].

For further information please read our article: Whose name should house insurance be in during probate?

There isn't a specific product called Executor Home Insurance; it's a term executors use when searching for insurance for an empty property in probate or for a property that is still occupied.

Some people call it executor house insurance or executor property insurance. Others search for probate home insurance, probate house insurance, or simply probate insurance. These all describe the same thing: specialist cover arranged in the name of the personal representatives while the estate is being administered.

There are very few specialist insurance providers, such as Insuristic, that offer a product specifically for insuring probate property.

If the property has up to 4 bedrooms, you don't know the rebuild value, you can get a quote based on the number of bedrooms. We will provide a blanket £750,000 buildings sum insured, which covers most residential properties, and if this is sufficient for the property, then you will have avoided underinsurance. If you do know the rebuild value, you may get a more accurate price, so use that instead.

If the property has more than 4 bedrooms, requesting a quotation based on the number of bedrooms will result in a referral to underwriters before a quotation is offered. A quotation based on an accurate rebuild figure will usually be quicker and more accurate than one based on the number of bedrooms.

As personal representatives, you are liable for any shortfall between the sum insured and the actual cost of rebuilding the property following a total loss. Provided £750,000 would be enough to rebuild the property, you are protecting yourself against the risk of underinsurance.

To understand the risk, read What Is The Risk Of Building Underinsurance In Probate?

You should never use the market value of the property for insurance as it can be completely different from the rebuild cost, which needs to reflect the cost of rebuilding it from scratch, including debris removal and professional fees. Getting this wrong could result in underinsurance and a significant financial loss for you.

To understand the risk, read What Is The Risk Of Building Underinsurance In Probate?

If the rebuild costs exceeds this amount, the quote will automatically refer to our underwriters, who will call you to offer advice and an appropriate Probate Property Insurance policy. It may differ from the one discussed on this page, but it will be suitable for your needs. The cover will be fully explained to you (and emailed to you to read) before you buy.

Contents are anything that is not fixed to the building, such as furniture, freestanding appliances, clothing, soft furnishings, and personal belongings. Fixed kitchen appliances, carpets, flooring and blinds are covered in the building's sum section of the policy. To work out how much cover you need, go through each room and estimate the cost to replace these items. Keep in mind the single article limit of £1,000 and the exclusions listed below when assessing what you need to insure.

No. Our Probate Property Insurance policy treats carpets, other flooring, and blinds as fixtures of the building. They should be included in the building's sum insured, not the contents. You do not need to add them to your contents figure.

Fixed or integrated appliances, such as a built-in oven, hob, an integrated washing machine, fridge or freezer, or a dishwasher, are treated as part of the building and are covered under the buildings section, up to £5,000 for any one loss. Freestanding appliances that are not fixed to the building should be included in the contents sum insured.

Cover above £30,000 is available on referral. Complete the online quote form, and we will arrange the appropriate level of cover for you offline. As you can imagine, contents in an empty property is a high theft risk, so if you are able to put items in safe storage it can reduce the risk and enable you to buy cover online if it then falls below £30,000.

The single article limit means that no individual item is covered for more than £1,000 under the contents section. If the property contains items worth more than £1,000 — such as a piece of furniture or a freestanding appliance — the policy will only pay up to £1,000 for that item in the event of a claim. This is one reason why high-value individual items such as jewellery and artwork are excluded entirely — see below.

Yes. The following are excluded from the contents section regardless of the level of cover you choose: jewellery, watches, furs, precious metals, artwork, antiques, money, and personal possessions. If the property contains items of this nature, they will need to be insured separately under a specialist policy.

Yes. The policy definition of buildings is broad and includes garages, outbuildings, car ports, walls, gates, fences, patios, terraces, drives and yards, as well as associated underground pipes and cables. You do not need to insure these separately — they form part of the buildings sum insured.

Walls and gates are included in the building's definition and are covered accordingly. However, it is worth noting that fences and gates are excluded from storm damage claims specifically — this is standard across most property insurance policies and is not unique to probate cover.

No. The policy specifically excludes property in the open. Contents must be within an enclosed part of the premises to be covered; items left outside in the garden, on the patio, or in any unenclosed area are not covered, regardless of the level of cover you choose. If the property has tools, garden furniture, or other items stored outside, these cannot be insured under this policy; they should be locked away in the premises or in safe storage.

Unlike standard home insurance, which typically limits cover for empty properties to 30 or 60 days, our Probate Property Insurance is specifically designed for properties that are unoccupied for extended periods. There is no fixed time limit; the policy covers the property for as long as the personal representatives are legally responsible for it, which can be months or, sometimes, a year or more, depending on the complexity of the estate. It is worth noting that the deceased's existing home insurance may remain valid for only 7 days after their passing, due to the change in risk notification condition, meaning specialist cover may be needed almost immediately.

You can insure for 3, 6, 9 or 12 months. Most executors choose 6 months as a starting point. Whatever duration you choose, you will get a renewal invitation approximately 20 days prior to expiry. You can renew the policy as often as is required, and if the property sells earlier than planned or the estate is settled sooner, provided there are no claims, you can cancel early and receive a pro-rata refund with no cancellation fee.

Probate timelines are unpredictable, and we understand that. If your policy is coming to an end and the estate has not yet been settled, you can renew for a further period. We would rather you contact us early so we can ensure there is no gap in cover.

Yes, if you reply to your renewal invitation requesting the changes you need, we will reissue the renewal quotation for you. It is common, for example, to request another 3 months at the end of a 6-month policy. Or perhaps the property is now empty of belongings, so the contents insurance is no longer required.

No. Receiving the Grant of Probate does not end your cover. The policy continues until the personal representatives are no longer responsible for the property, which is typically when it is sold, transferred to a beneficiary, or occupied again. Many executors continue to need cover for months after probate is granted while the property is being prepared for sale.

Yes. Our shortest policy term is 3 months. If you need cover for less than 3 months, a 3-month policy is still your best option — if the property sells or the estate is settled sooner, you can cancel early and receive a pro-rata refund with no cancellation fee, provided no claim has been made.

Our minimum policy term is 3 months, so a single month is not available as a standalone option. However, if you take out a 3-month policy and no longer need it after one month, provided you haven’t claimed, you can cancel, and we will refund the remaining two months pro rata with no cancellation fee.

We will send you a renewal invitation before your policy expires, but if cover lapses there will be a gap in protection during which any loss would be uninsured and the personal representatives would be personally liable. If your policy has lapsed in error, you can log in to your portal to requote your renewal — you will need to declare that the property has not been continuously insured as part of the process. If you are unsure what to do, contact us and we will help you get cover back in place as quickly as possible.

You can cancel your policy at any time by replying to the email you received with your policy documents or from our Customer Support page. If you are within the 14-day cooling-off period and the policy did not meet your needs, and you have arranged alternative cover, we can cancel from the start date and treat it as if it never existed, provided no claims have been made. If you have used the cover but no longer need it, we will cancel from the current date and issue a pro-rata refund with no cancellation fee.

You should cancel at completion, not exchange. Until completion, the sale can still fall through and the property remains the responsibility of the personal representatives. Cancelling at exchange leaves the estate exposed if the sale does not proceed. Do not request cancellation in advance of completion even if you know the completion date — delays are common in conveyancing and could leave the property uninsured. Once completion has taken place and the property has legally changed hands, contact us to cancel and we will issue a pro-rata refund for any unused premium, with no cancellation fee, provided no claims have been made.

Yes, provided no claims have been made. Unlike many insurers, we do not charge cancellation fees or retain a minimum amount of unused premium. You will receive a pro-rata refund for any unused time remaining on your policy. If a claim has been made, no refund is due.

You can cancel the policy at any time, but if a claim has been made no refund of premium will be due. The policy will simply run to its cancellation date without a refund.

Properties in a poor state of repair cannot be quoted online, but complete our online quote form, and our underwriters will help you find a solution with a non-standard home insurer. Cover will differ from what is on this page and will be fully explained to you before you buy.

Boarded-up properties cannot be quoted online, but complete our online quote form, and our underwriters will help you find a suitable solution with a non-standard home insurer.

Yes. Our online quote system covers non-structural renovation works costing less than £50,000. If the works are structural, or the cost exceeds £50,000, the quote will refer to our underwriters who will provide advice and a bespoke solution suited to the scale of the project.

Yes, but this cannot be quoted online. All commercially used properties are referred to our underwriters for an advised quote. Complete our online quote form and we will be in touch to discuss the right solution for you.

This cannot be quoted online. Properties that have been empty for an extended period present a greater challenge to insure, as insurers are concerned about the maintenance and condition of a property that has been unoccupied for so long. Many will have been boarded up by this point. The market for this type of risk is more limited, but complete our online quote form and our underwriters will call you to discuss your requirements and provide an advised quote.

Properties in flood areas cannot be quoted online, but complete our online quote form, and our underwriters will help you find a suitable policy.

Yes. A property being marketed for sale does not affect the cover in any way, provided it is still in the care of the personal representatives and hasn’t been inherited i.e. title deeds transferred to a beneficiary it can be covered on this policy. The personal representatives are still legally responsible for the property until the sale completes, so cover should be maintained throughout. When the sale completes, you can cancel the policy and receive a pro-rata refund of any unused premium, with no cancellation fee, provided no claim has been made.

Yes, provided the people living there are doing so with the permission of the executors (if there's a Will) or the administrators (if there isn't) – generally called personal representatives.

Cover can often be arranged, but it's very different to the cover explained on this page and is more involved than insuring an empty probate property, and standard policies rarely fit.

If the property is occupied without the personal representatives' permission, they are effectively squatting, and most insurers will decline to insure it due to concerns about malicious damage and theft.

Why don’t the occupants have insurable interest?

Under the Administration of Estates Act 1925, legal ownership of the property passes temporarily to the personal representatives, not to the beneficiaries (often the occupants) who may inherit later. In practice, that means the executors or administrators hold the insurable interest, and the occupants, even if they're beneficiaries, usually can't legally insure the property themselves.

Why isn't standard home insurance suitable?

Standard home insurance is usually the wrong fit, and most insurers will decline to offer it. There are three reasons: the occupants can't arrange cover because they have no insurable interest; insurers tend to treat occupants who don't own the property as a higher risk, on the basis that they may take less care of it; and because the legal owners (the executors or administrators) don't live there, the risk looks nothing like a normal homeowner's policy.

Will standard landlord insurance work instead?

Usually not. Most landlord policies require a formal tenancy agreement as a condition of cover, so unless the deceased already let the property out on that basis and insured it accordingly, a landlord policy won't respond, even where people are living there with your permission. It's a common assumption, and an expensive one to get wrong.

The exception is where the property was already rented out under a formal tenancy before death, and that tenancy is continuing. The existing landlord policy may then be transferable, but don't assume it carries over automatically. Speak to the insurer or broker straight away, and make sure the policy is updated to show the estate as the owner.

If you need advice on arranging landlord cover, contact us, and we'll arrange a quote.

How do I get the right cover for an occupied probate property?

Because the property is occupied, the cover and policy conditions are completely different from the Probate House Insurance set out on the rest of this page, which is designed for empty properties. An occupied probate property sits much closer to a standard home insurance policy, so the unoccupied conditions described above won't apply in the same way. Our underwriters will explain exactly what's covered and what's required during the quotation, so it's all clear before you buy.

We've developed a specialist solution with our underwriters that:

It protects you from personal liability and makes sure the property is properly covered.

You can request a quote here.

This is a very difficult risk to insure and it is unlikely any insurer will offer cover in this situation. The risk of malicious damage and theft is considered too high whilst an eviction is in progress. The best course of action is to progress the eviction as quickly as possible and contact us once the property is vacant — we can then arrange appropriate cover promptly.

Yes, although many insurers will decline in this situation. We will quote, provided you can confirm the property has been inspected within the last 7 days and there is no existing damage that could give rise to a claim. If we proceed, a restriction will apply for the first 7 days of the policy that states storm, flood, and escape-of-water claims will not be covered during this initial period. Subsidence, ground heave or landslip that originated before the policy started is also excluded, regardless of whether the damage was known about at the time. These restrictions exist because insurers need to protect against someone insuring a property after damage has already occurred.

Potentially, if the existing insurer can no longer quote, this requires an advised quote from our underwriters rather than an online quote. Submit our quote form and an underwriter will be in touch. The property will need to be windproof, water-tight, and secure. Complete our online quote form and we will be in touch to discuss the right solution for you.

Cracks can indicate subsidence, which requires specialist underwriting. You need to declare this at the quotation stage. We won’t be able to quote online. Once you submit the quote form, our underwriters will provide advice and an appropriate solution. Do not ignore cracks, as uninsured subsidence damage is a costly risk that a personal representative can face.

Yes. We will quote online for all properties that were built from 1800 onwards, provided they meet our standard construction requirements (walls of Brick or Stone and roofs of slate and tile).

If there have been claims in the last 5 years, this will refer to the underwriter once you submit the quote. They will then call you to discuss and provide an advised quote.

The 30-day inspection requirement is a condition of this policy, but it is worth remembering that anyone with a key can carry out the inspection — it does not have to be the executor or administrator. A neighbour, friend, family member, or local tradesperson can visit on your behalf, take the required photos, and send them to you. If you genuinely cannot arrange an inspection every 30 days by any means, complete our online quote form and our underwriters will be in touch — there are limited options available for less frequent inspections, though these are not available online.

If the estate is being administered by a solicitor, ask them about Probate Pro, our solicitor solution which includes inspection-free cover.

It is a policy condition that the property is adequately secured against unauthorised entry at all times. In practice, this means all external doors must be locked and all accessible windows must be lockable and locked when the property is unoccupied. We do not specify a lock type, nor that windows need to have a key, just be lockable. Failure to comply could mean a claim arising from illegal entry is declined.

Read this page to learn more: What Is Insuristic's Unoccupied Home Minimum Security Requirement?

Yes. Removing junk mail, newspapers and flyers during each inspection is a policy condition — failure to do so could mean a fire claim is not covered. Diverting post to one of the personal representatives is the most reliable way to prevent accumulations building up between visits, and it also ensures important correspondence about the property or estate is not missed.

Each inspection must cover both the interior and exterior of the property. It is a policy condition that all accumulations of combustible materials, including junk mail, newspapers and flyers, are removed during every inspection, as a build-up of these indicates the property is empty (and a bigger target for thieves and vandals), as well as posing a fire risk, and failure to remove them could affect a fire claim. You should also check for maintenance issues and quickly resolve them to prevent loss. Use a mobile device to take one photo of the exterior and one of the interior to evidence the visit. The date and time are automatically recorded in the image. These photos will be required by our underwriters' claims team in the event of a claim.

A missed inspection can automatically invalidate your policy for claims arising from a gap in inspections that are relevant to the loss. The policy places the burden on you to prove that the lack of inspection did not cause or contribute to the damage claimed, otherwise your claim could be denied. The practical answer is to inspect in line with the policy condition and never let inspections lapse for extended periods.

The inspection images are your evidence in the event of a claim and the policy requires you to present them if asked. To reduce the risk of a lost device it may be worth considering storing these in the cloud or transferring a copy to another device. If you have lost images from a previous inspection, make sure your next visit is thoroughly documented and keep records going forward. You may want to take more images to back up the fact there were no issues with the property.

Yes, and if you are not draining the water system, you must do so between 1st October and 31st March. It is a policy condition that all other services are switched off at the mains when the property is unoccupied, but gas and electricity are specifically exempt where needed to maintain heating or security. Outside of the winter period, if the system has been drained, utilities should otherwise be switched off.

If you are relying on the heating to maintain escape of water cover between 1st October and 31st March, failing to keep the heating running continuously at a minimum of 15°C, leaving the loft hatch open, could mean an escape of water or burst pipe claim is excluded. This is a policy condition, and the heating must not be controlled by a timer during this period. If maintaining the temperature is proving difficult, draining the system is the more reliable option and removes the condition and the risk entirely.

Read this page to learn more: Do I have to drain the water system with Insuristic’s Probate Property Insurance?

Yes. Electricity may remain on to power an active intruder alarm, fire alarm, or external security lighting. This is a specific exception within the utilities condition, which otherwise requires all services to be switched off at the mains when the property is unoccupied.

No. The policy requires all services to be switched off at the mains when the property is unoccupied. Electricity may only remain on to power heating or an active security system such as an intruder alarm or fire alarm. Lights on timers can present a fire risk and therefore do not fall within either exception, so the electricity would need to be switched off at the mains when you leave the property.

It is a policy condition that all services are switched off at the mains when the property is unoccupied, except where gas and electricity are needed for heating or security. Leaving them on unnecessarily increases the risk of fire or explosion, and if a claim arises from an incident that could be linked to utilities being left on in breach of this condition, the claim could be declined.

Yes — this is a policy condition, and you should tell us during the quotation stage if these are planned. If your plans change and you haven't previously notified us, you must notify us at least 7 days before any structural works of any value commence, or any non-structural works with a cost exceeding £50,000. Structural works are defined as any works involving changes to the roof or load-bearing walls. You must also notify us of any application for planning permission or any planned demolition. If you are unsure whether your works require notification, contact us before they start — it is always better to check. When notified, we may amend the terms or premium of your policy, or cancel your policy in accordance with the cancellation condition.

Yes, it is a policy condition that the building and gardens of the property are kept in a suitably maintained condition. An overgrown or neglected garden is one of the clearest signals that a property is unoccupied, increasing the risk of theft and vandalism. During each inspection, check the condition of the grounds and the building, and address any obvious maintenance issues promptly.

If you are relying on the heating to satisfy the winter escape of water condition between 1st October and 31st March, a heating system failure means you are no longer complying with the condition and escape of water cover will be affected until it is restored. If the heating fails, you should consider draining the system immediately to prevent loss as there is no cover for escape of water until either the heating is restored and running continuously at 15°C (with the loft hatch open). This is why having the heating system serviced before winter is strongly recommended.

Because the policy is arranged in the name of the estate rather than any individual, a change of executor or administrator does not affect your cover. Whether an executor steps down, loses capacity, or is replaced, the policy remains valid — it belongs to the estate, not the person. This is one of the reasons why getting the insured name right from the outset is so important.

The cost of insuring the property during probate is an expense of the estate and is paid from the estate's funds. It is not a personal cost to the executors or administrators, though they are personally responsible for ensuring the property is adequately insured. If estate funds are not immediately available, the personal representatives may need to fund the cost initially and recover it from the estate once funds are released.

The responsibility passes immediately to the personal representatives — the executors if there is a Will, or the administrators if there isn't. Standard home insurance arranged by the deceased should be reviewed urgently as it may no longer provide adequate cover, and specialist probate property insurance should be arranged as soon as possible to protect the personal representatives' liability.

You can get a quote online from Insuristic in around two minutes. The policy should be arranged in the name of the executors or administrators of the estate — not in the name of the deceased. You will need the property address, an estimate of the rebuild value or the number of bedrooms, and the names of the personal representatives. If the property has any non-standard features, our team can arrange cover offline.

There is a 14-day cooling-off period from the date the policy is issued. If the policy did not meet your needs and you have arranged alternative cover, we can cancel it from the start date and treat it as if it never existed, provided no claims have been made.

If you have used the cover but no longer need it — for example the property has sold or become occupied — we will cancel from the current date and issue a pro-rata refund with no cancellation fee.

The excess is the amount the estate contributes towards a claim (rather than from the personal representative's funds) before the insurer pays the remainder. The excess varies depending on the type of claim: £250 for standard claims and flood, £500 for escape of water, and £1,000 for subsidence.

If a claim falls outside the cover you have purchased, the loss passes to the personal representatives to fund personally — which is why choosing the right level of cover from the outset is so important. Bronze cover, for example, does not include burst pipes, theft, flood or storm damage. In our experience, most executors buy at least Silver. Buying as much cover as possible may be a wise choice.

When someone dies, ownership of their property passes immediately to their estate. The personal representatives — executors if there is a Will, administrators if there isn't — become legally responsible for the property and for insuring it. Beneficiaries do not own the property until it has been formally transferred to them following the completion of probate. Read our full guide: Who owns and insures a house during probate?

It depends on how the property was owned. If the property was owned solely in the name of the person who died, probate will be required before contracts can be exchanged. The property can be marketed and an offer accepted before probate is granted, but the sale cannot complete without it. If the property was jointly owned as joint tenants, it passes automatically to the surviving owner without the need for probate. If jointly owned as tenants in common, probate is likely to be required. If you are unsure how the property is owned, a search of the Land Registry will confirm this. For advice on your specific situation, speak to a probate solicitor.

We cover all types of houses — both two and three-storey, bungalows, barn conversions, and most other residential property types. Flats are not available online but can be arranged offline. Standard construction properties can be quoted online in around two minutes. Non-standard construction — such as timber frame, steel frame, concrete walls or non-standard roofs — can be arranged offline through our underwriters. The only property type we cannot cover is an empty property with a thatched roof.

Standard construction means brick or stone walls with a tile or slate roof. If your property meets this description, you can get a quote online. If the walls or roof are of a different construction, complete our online quote form and our underwriters will call you to arrange an appropriate policy.

Yes, and unlike many insurance providers, we do not ask you to declare what percentage of the roof is flat, which catches out many executors who simply don't know. We do require evidence of a roof inspection within the last 5 years confirming the roof is wind and watertight. If you don't know whether the deceased arranged one, you should organise an inspection as soon as possible. A specialist roofing company can carry this out relatively inexpensively.

Listed buildings cannot be quoted online due to the specialist nature of the rebuild requirements, but complete our online quote form and our underwriters will help you find a suitable solution. Cover will differ from what is on this page and will be fully explained to you before you buy.

Concrete wall construction cannot be quoted online, but complete our online quote form and our underwriters will call you to discuss your requirements and arrange an appropriate policy.

If the barn conversion is of standard construction — brick or stone walls with a tile or slate roof — it can be quoted online. If the construction is non-standard, complete our online quote form and our underwriters will call you to arrange an appropriate policy.

Not online. Most flats we see in probate are already insured under a building management company's block policy, which often continues regardless of the change of ownership. Complete our online quote form, and our underwriters will call you to discuss whether separate cover is needed and arrange it if so.

Timber frame construction cannot be quoted online, but complete our online quote form and our underwriters will call you to discuss your requirements and arrange an appropriate policy.

Yes, potentially. A property with a thatch roof is high risk because fire spreads quickly and can often take the whole building with it, and that risk is even higher when a property is standing empty with no one to spot a problem early. Not many insurers will quote on it, but our underwriters work with ones that can consider it. The cover and conditions will be different from the rest of this page, and they'll explain exactly how when they talk through your quote. Submit your details, and our underwriters will be in touch.

No, our policy covers properties in England, Scotland and Wales only. If the probate property is in Northern Ireland, you will need to contact a local insurance broker who specialises in the Northern Ireland market. The British Insurance Brokers' Association (BIBA) broker finder can help you locate a suitable broker in your area.

Steel frame construction cannot be quoted online, but complete our online quote form, and our underwriters will call you to discuss your requirements and arrange an appropriate policy.

Pre-fabricated properties cannot be quoted online, but complete our online quote form and our underwriters will call you to discuss your requirements and arrange an appropriate policy.

Concrete roofs cannot be quoted online, but complete our online quote form and our underwriters will call you to discuss your requirements and arrange an appropriate policy.

Green roofs cannot be quoted online, but complete our online quote form and our underwriters will call you to discuss your requirements and arrange an appropriate policy.

This cannot be quoted online, and it may be the insurance needs to remain with the existing insurer – so you should talk to them first and make a claim if you haven’t already. Complete our online quote form and our underwriters will call you to discuss your requirements. If cover is available, they will arrange an appropriate policy and explain the terms fully before you buy.

This cannot be quoted online. Complete our online quote form and our underwriters will call you to discuss your requirements. If cover is available, they will arrange an appropriate policy and explain the terms fully before you buy.

Yes. Swimming pools are included within the definition of buildings under this policy and are covered as part of the buildings sum insured. You do not need to insure them separately. When estimating the rebuild value, make sure the cost of the pool is reflected in the buildings sum insured.

Rob Faulkner is the founder of Insuristic and an expert in Probate Insurance, Legal Indemnity and Unoccupied Home Insurance with 30 years’ experience in the UK insurance market. He is also a member of the judging panel for The British Wills and Probate Awards 2026.

Rob is an ACII Chartered Insurance Broker, a Chartered Manager, and a Member of the Chartered Institute of Marketing. His background spans insurers, brokers, and Insurtechs, always focused on innovation, transparency, simplicity, and fair value.

Rob is passionate about product development and improving insurance education through marketing, helping people understand what they are buying. These values sit at the heart of everything we do at Insuristic.

His mission is to make Insurance smarter, easier to understand, and faster to buy. Particularly for the Probate market, where Rob has identified friction points and solved them for lay clients and solicitors alike.

Want to learn more? Visit my author page or follow me on LinkedIn.

Insuristic Limited is an Appointed Representative of SJL (Worcester) Ltd, who are authorised and regulated by the Financial Conduct Authority with the reference number 991835. This can be checked by visiting https://register.fca.org.uk/s/.

Registered Office: Unit 2, 262 Walsall Road, Cannock, England, WS11 0JL. Registered in England and Wales No: 13926650.

Insuristic is a registered trademark. ©Copyright 2023 Insuristic Limited. All Rights Reserved.