Whilst Probate House Insurance isn’t compulsory in the same way as insuring your car, specialist cover should be viewed as a priority by the Personal Representatives due to the significance of their personal liability for declined claims resulting from gaps in cover or underinsurance.

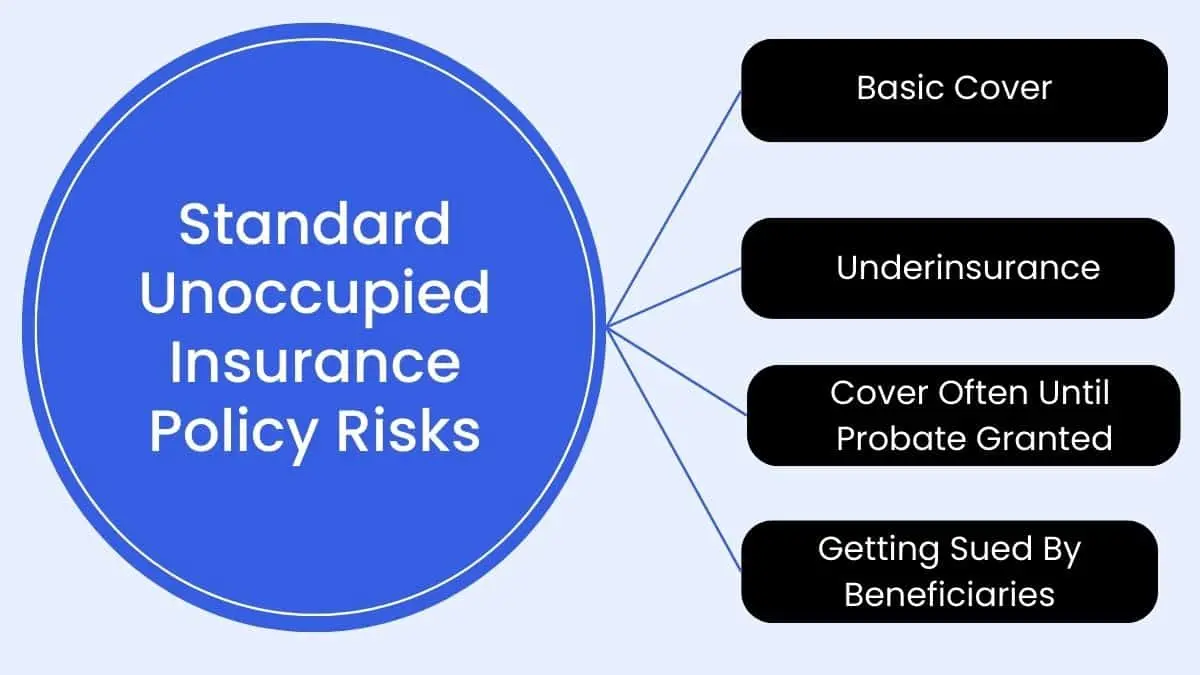

The common risks you might face are:

If you bought a standard policy that excludes claims like a burst pipe, theft, vandalism, subsidence, flood and more, if a claim comes in, it wouldn’t be the estate that funds repair or replacement of property it would be the personal representatives responsible for insuring it. In fact, the beneficiaries are legally entitled to sue all the personal representatives to recover the lost value of their inheritance.

So insuring with a Probate specialist like Insuristic can make a lot of sense and be a safer option.

We have designed a policy specifically for empty Probate in probate and to protect the liability of the people responsible for insuring it.

Our policy is not a rebadged copy of a standard unoccupied home insurance policy.

You will find the cover, the information we provide, and the questions we ask are all specific to probate.

Our cover options are broad to help you protect your liability and can be bought short-term, or annually, from the point someone passes away until the property is sold, occupied again or inherited.

Plus, we know it's hard to know when the Probate process ends. So to help you avoid paying too much for property insurance, we have a really fair approach to cancellations that you may not find anywhere else.

If you need to cancel earlier than planned, provided you haven’t claimed, there are no cancellation fees, and you get back the value of any unused time on cover.

To find out more about our cover or get a quote, visit our Probate House Insurance page. If you have further questions, visit our Probate Insurance FAQs page.

Rob Faulkner is a leading expert in Probate Insurance, Probate Risk Management, Property Insurance (especially Unoccupied Home Insurance), with nearly 30 years’ experience in the UK insurance market. He is the founder of Insuristic, a specialist provider of probate-related insurance solutions and educational content for executors.

Rob is an ACII Chartered Insurance Broker, a Chartered Manager, and a Member of the Chartered Institute of Marketing. His background spans insurers, brokers, and Insurtechs, always focused on innovation, transparency, simplicity, and fair value.

Rob is passionate about product development and improving insurance education through marketing, helping people understand what they are buying. These values sit at the heart of everything we do at Insuristic.

His mission is to make Insurance smarter, easier to understand, and faster to buy. Particularly for the Probate market, where Rob has identified friction points and solved them for lay clients and solicitors alike.

Want to learn more? Visit my author page or follow me on LinkedIn.

Insuristic Limited is an Appointed Representative of SJL (Worcester) Ltd, who are authorised and regulated by the Financial Conduct Authority with the reference number 991835. This can be checked by visiting https://register.fca.org.uk/s/.

Registered Office: Unit 2, 262 Walsall Road, Cannock, England, WS11 0JL. Registered in England and Wales No: 13926650.

Insuristic is a registered trademark. ©Copyright 2023 Insuristic Limited. All Rights Reserved.