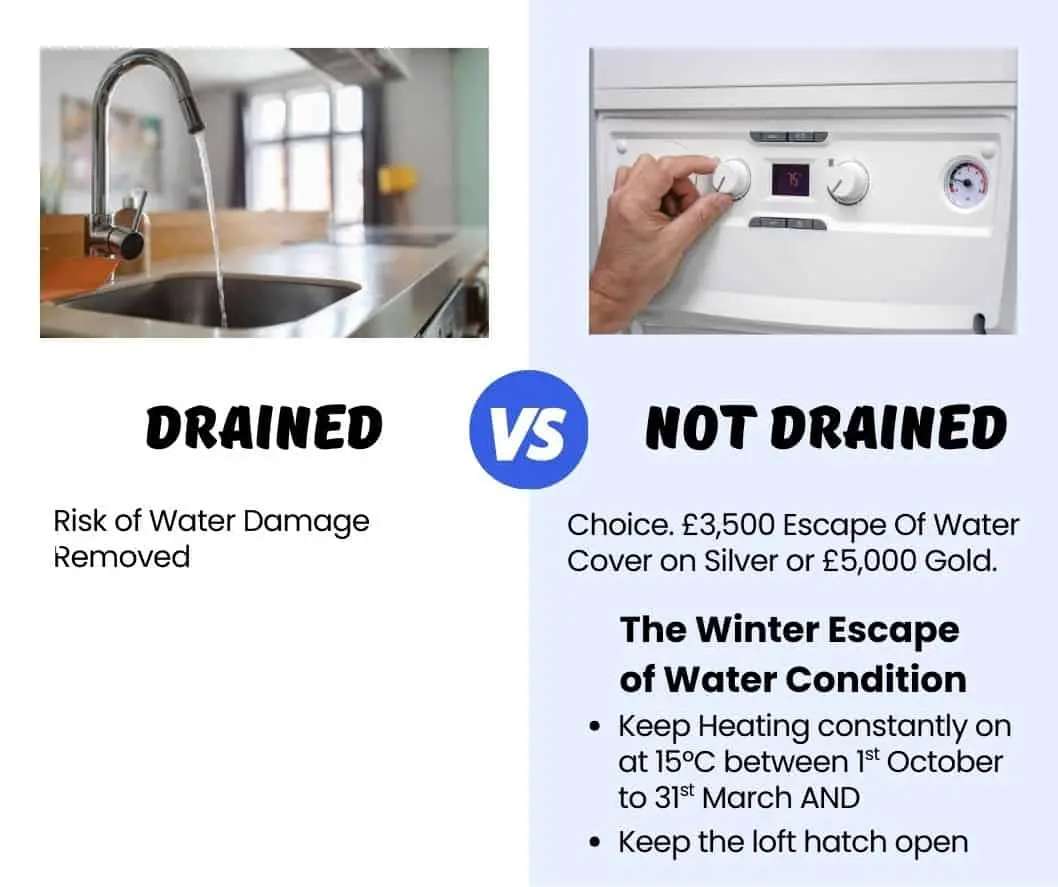

We provide protection against the sudden escape of water on both our Silver and Gold cover options, but how you comply with the policy conditions depends on how you assess the risk and your intentions at the property.

We know that sometimes draining water systems isn’t an option.

Maybe you need to keep the heating on during the winter so the property is inviting to potential buyers.

Perhaps you have employed a gardener to maintain the gardens, keeping the property looking smart and as if it is occupied, thereby reducing the risk of break-ins. We know draining water wouldn’t be practical.

The challenge for insurers and policyholders is that burst pipes are the biggest cause of loss. So you will see many insurance providers not offering the cover at all, or where they do, with restrictions to minimise the loss.

From a personal representative's perspective, the last thing you need is an undetected burst pipe that can go undetected for weeks, as this can cause significant damage and seriously set back your plans for the property whilst the damage is rectified.

Standard Unoccupied Home Insurance policies often provide no cover for escape of water, leaving this cost to the personal representatives to fund in the event of an issue. It is unlikely the beneficiaries will be happy for the estate to fund this loss, as it could have been insured on a more specialist policy.

So burst pipe events are a big risk for the personal representatives, and, as our most common cause of claim, they are reasonably frequent, with high reinstatement costs.

Please note: The Bronze cover does not include cover for Escape of Water claims.

If you plan not to drain the water system, consider the following risk management tips:

I hope this helps you.

To find out more about our cover or get a quote, visit our Probate House Insurance page. If you have further questions, visit our Probate Insurance FAQs page.

Rob Faulkner is a leading expert in Probate Insurance, Probate Risk Management, Property Insurance (especially Unoccupied Home Insurance), with nearly 30 years’ experience in the UK insurance market. He is the founder of Insuristic, a specialist provider of probate-related insurance solutions and educational content for executors.

Rob is an ACII Chartered Insurance Broker, a Chartered Manager, and a Member of the Chartered Institute of Marketing. His background spans insurers, brokers, and Insurtechs, always focused on innovation, transparency, simplicity, and fair value.

Rob is passionate about product development and improving insurance education through marketing, helping people understand what they are buying. These values sit at the heart of everything we do at Insuristic.

His mission is to make Insurance smarter, easier to understand, and faster to buy. Particularly for the Probate market, where Rob has identified friction points and solved them for lay clients and solicitors alike.

Want to learn more? Visit my author page or follow me on LinkedIn.

Insuristic Limited is an Appointed Representative of SJL (Worcester) Ltd, who are authorised and regulated by the Financial Conduct Authority with the reference number 991835. This can be checked by visiting https://register.fca.org.uk/s/.

Registered Office: Unit 2, 262 Walsall Road, Cannock, England, WS11 0JL. Registered in England and Wales No: 13926650.

Insuristic is a registered trademark. ©Copyright 2023 Insuristic Limited. All Rights Reserved.